Gimmerton/E+ via Getty Images

Sometimes, the best returns come from investing in companies that may not seem to offer significant upside potential solely because of the industry in which they operate. One really good example that I could point to in this regard is John B. Sanfilippo & Son (NASDAQ:JBSS), a processor and distributor of peanuts, pecans, cashews, walnuts, almonds, and other nuts that it sells in the US. Over the past year, shares of the company have skyrocketed, driven by continued growth and the fact that shares of the business looked cheap back then. Fast forward to today, and the picture is not quite as attractive. The easy money has certainly been made and the stock is looking more or less fairly valued. Given these developments, and in spite of a stellar year, I have decided to downgrade the company from a 'buy' to a 'hold' to reflect my new view that the stock should perform more or less along the lines of the broader market for the foreseeable future.

What a year it has been

A little over a year ago, on July 18th of 2022, I published a bullish article talking about the upside potential that John B. Sanfilippo & Son offered investors. At that time, I acknowledged the firm as an interesting business that had a history of stability but that struggled when it came to achieving growth. Performance most recently at that time had been mixed, but the overall fundamental picture for the company was positive. Add on top of this how shares were priced, and I had no problem rating the business a 'buy' to reflect my view at the time that shares should outperform the broader market moving forward. Since then, management has absolutely delivered. While the S&P 500 is up 16.8%, shares of John B. Sanfilippo & Son have skyrocketed 59.3%.

Author - SEC EDGAR Data

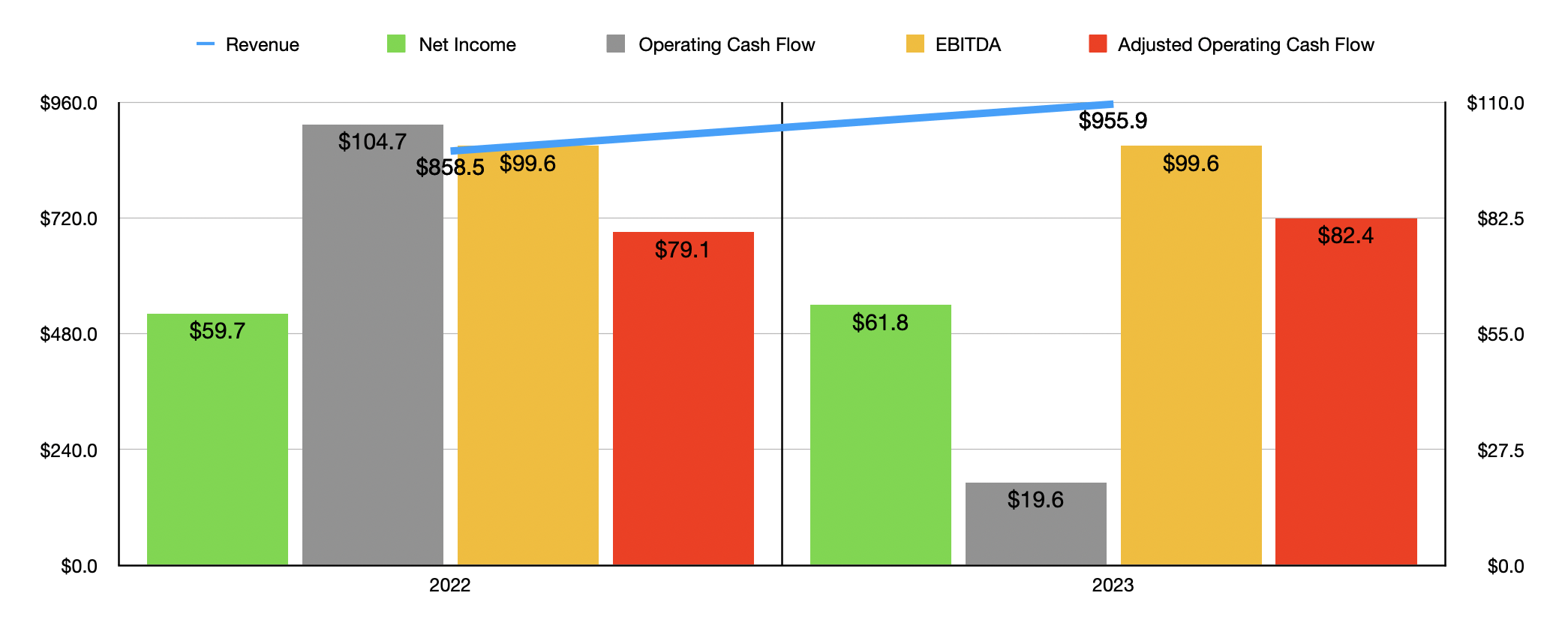

Even though I found myself bullish on the company at that time, I would not have imagined that shares had such upside potential behind them. I would have thought outperforming the market by 10% to 15% would have been sufficient. But the company even surprised me. And it did so with fundamental performance that, while attractive, was not shockingly strong. To see what I mean, let's first focus on how the firm performed during its 2023 fiscal year. During that time, revenue came in at $955.9 million. That represents an increase of 11.3% over the $858.5 million the company reported one year earlier. This increase in sales was, according to management, driven by a combination of higher volume and higher product pricing. Shipment volumes jumped 6.9% year over year while the weighted average selling price per pound of nuts that the company sold grew 4.2%.

On the bottom line, the picture was somewhat mixed, but mostly positive. Net income inched up from $59.7 million to $61.8 million. Those who are bearish about the company might point out the fact that operating cash flow declined from $104.7 million to $19.6 million. But if we adjust for changes in working capital, we would get an increase from $79.1 million to $82.4 million. And finally, EBITDA for the business managed to remain flat at $99.6 million.

Author - SEC EDGAR Data

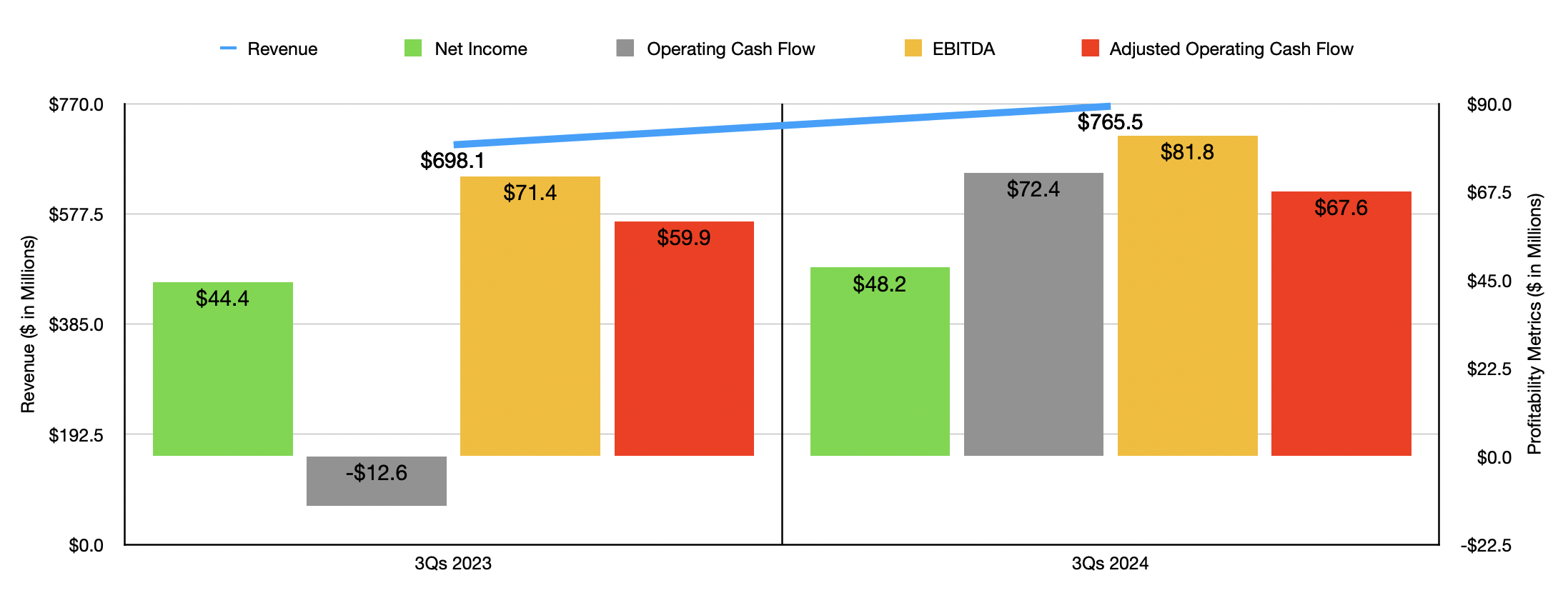

When it comes to the 2024 fiscal year, management has provided data covering three different quarters. Sales continued to climb, with revenue of $765.5 million beating out the $698.1 million reported the same time last year. This increase, totaling about 9.7% year over year, can be attributed to a 0.8% increase in sales volume. But the heavy lifter has been increased pricing, with the weighted average selling price per pound of product sold jumping 8.8% year over year.

On the bottom line, the picture improved, with net income climbing from $44.4 million to $48.2 million. In addition to benefiting from the increase in sales, the company also benefited from a decrease in its selling expenses relative to revenue. These costs went from 8.1 percent of sales during the first nine months of the company's 2024 fiscal year to 7.6% the same time this year. Although this may not seem like a huge change, it did help the company's bottom line to the tune of about $3.8 million on a pre-tax basis. This improvement was driven largely by a $2.1 million decrease in freight expenses because of a decrease in freight rates, and by a $1.7 million drop in advertising, consumer insight research, and related consulting expenses.

Other profitability metrics for the company followed a similar trajectory. Operating cash flow, for instance, shot up from negative $12.6 million to $72.4 million. If we adjust for changes in working capital, however, the increase would have been more modest, but still respectable, climbing from $59.9 million to $67.6 million. Over the same window of time, EBITDA for the company grew from $71.4 million to $81.8 million.

Author - SEC EDGAR Data

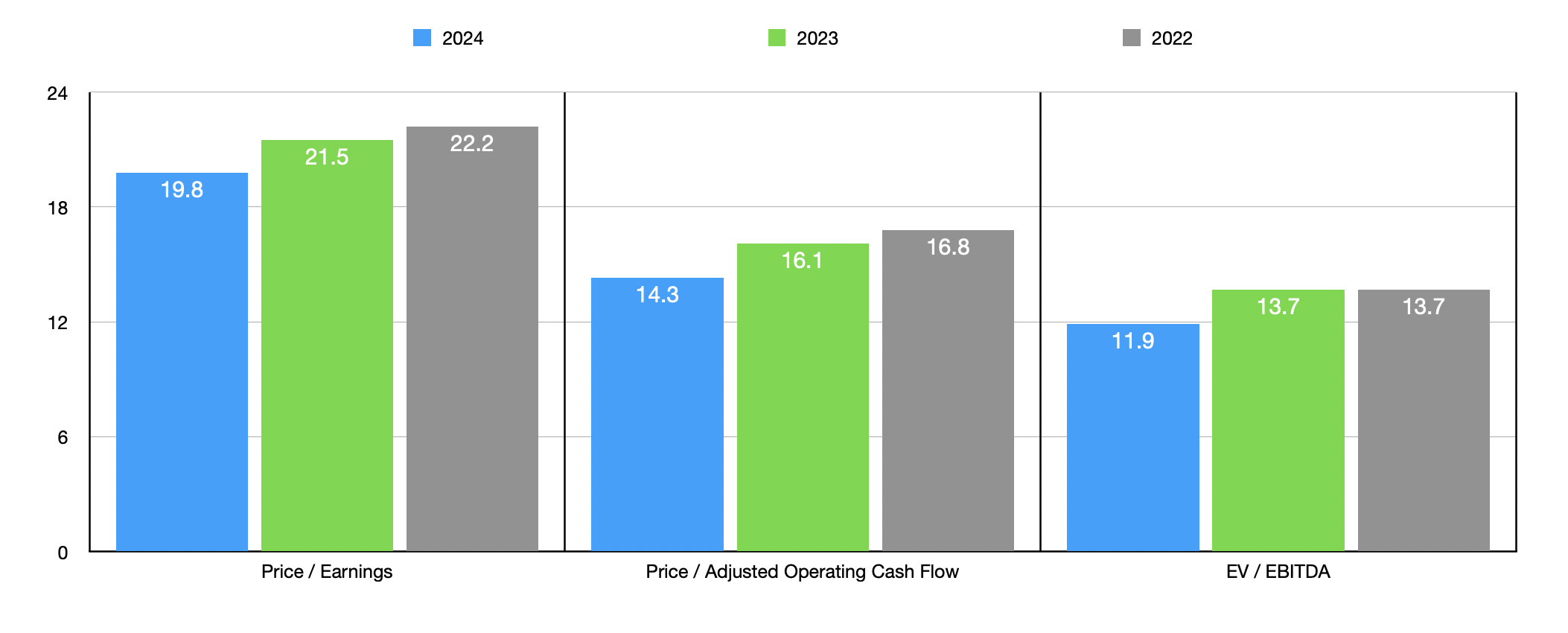

If we annualize the results experienced so far for the 2024 fiscal year, we would get net income of $67.1 million. The adjusted operating cash flow would be about $93 million, while EBITDA would come in at $114.1 million. Using these figures, valuing the company becomes quite simple. As you can see in the chart above, shares are priced using the forward estimates. They are also priced using data from 2022 and 2023. For the most part, the stock doesn't look bad. This is especially true when it comes to the EV to EBITDA multiple that it's trading for. But it's definitely not in value territory anymore. As part of my analysis, in the table below, I also compared the company to five similar firms. In each case, three of the five companies ended up being cheaper than John B. Sanfilippo & Son.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| John B. Sanfilippo & Son Inc. | 19.8 | 14.3 | 11.9 |

| Adecoagro SA (AGRO) | 17.9 | 3.5 | 4.2 |

| Mission Produce (AVO) | 48.6 | 18.4 | 212.9 |

| Dole (DOLE) | 12.1 | 3.1 | 7.6 |

| The Hain Celestial Group (HAIN) | 33.2 | 156.2 | 16.1 |

| Post Holdings (POST) | 13.6 | 12.9 | 9.3 |

Takeaway

From what I can tell, John B. Sanfilippo & Son is doing a fine job. The company has, from a share price perspective, outperformed my expectations. Fundamental performance has not been exactly stellar. On the other hand, it has definitely been positive. When you add in the improvement in the firm's top and bottom lines to how shares are priced both on an absolute basis and relative to similar firms, I would argue that now might be a good time to downgrade the company from the 'buy' I had it at previously to a 'hold' today.

"behind" - Google News

July 25, 2023 at 05:39PM

https://ift.tt/lDrbK5R

John B. Sanfilippo & Son: Nutty Returns Are Behind Us (NASDAQ:JBSS) - Seeking Alpha

"behind" - Google News

https://ift.tt/05iAQSK

https://ift.tt/ZX15hwK

Bagikan Berita Ini

0 Response to "John B. Sanfilippo & Son: Nutty Returns Are Behind Us (NASDAQ:JBSS) - Seeking Alpha"

Post a Comment